06th December 2019

06th December 2019

A fundamental misconception of risk is causing many shippers of ocean freight to completely overlook the need for cargo insurance of any kind and to cover against a multitude of eventualities.

Many industry professionals fear the endemic perception that insurance is unnecessary or not worth the expense is unlikely to change in the foreseeable future.

One estimate is that more than 90 per cent of all cargo imported into the United States (US) does so without any insurance, according to the US-based Association for Trade Compliance (ATC).

Steve Fodor, Director of the ATC said that cargo insurance costs less than half a per cent of the shipments value, on average most importers don’t purchase coverage, according to an article in Insurance Marine News.

There are also misconceptions that most products are purchased on a ‘Free on Board’ (FOB) basis, in this case supplier is not required to provide insurance coverage.

There are also two types of FOBs: FOB Destination and FOB Origin. Shippers are responsible for coverage if the buyer takes out FOB Destination, but in many cases, are unaware of this responsibility.

Even if the freight is moved under cost, insurance and freight (CIF) terms, where the seller is required to arrange for carriage of goods by sea to a port of destination, goods are only insured to the first destination port and do not cover any damages or losses incurred after that point.

The idea that nothing goes wrong is also a dangerous game to play, as higher supply chain risk from accidents, extreme weather and cargo crime are all on the increase. It does not make good commercial sense to lose thousands of dollars just to save on a small insurance premium.

This lack of understanding of the need for adequate insurance coverage by many in the shipping sector has long been a source of frustration for insurance professionals, including those based at the Through Transport Mutual Services (UK) Ltd. (TT Club), a leading provider of insurance provisions to the international transport and logistics industry.

Peregrine Storrs-Fox, Risk Management Director of TT Club said, “We are aware that a proportion of cargo is transported without ‘all-risks’ cover. Analyses will differ as to what that proportion may be, influenced by the type of entity involved in shipping and the nature of the commodity,” told Forward with Toll news website.

Storrs-Fox added, “There may well be a lack of knowledge of the contractual liability exposure and therefore an expectation that full recovery will be achieved.”

He explained why the sector needs to be more alert to this issue, “Understanding risk requires appreciation far beyond the pure value of the goods being transported. The shipper community needs to consider the general and regulatory information available to optimise the likelihood that goods are received in good order.”

He referred to the doctrines laid out in the principles of the Code of Practice for Packing of Cargo Transport Units (CTU Code), and of the importance of complying with dangerous goods regulations.

However, despite these codes and warnings of the consequences many times over of the failure to adopt proper insurance provision, Storrs-Fox remains pessimistic about changing industry thinking.

He lamented, “I cannot foresee any material change in the cargo insurance buying habits of shippers, although an increasing number of shippers are taking out cargo insurance as awareness of growing supply chain risk continues to rise.”

In response to the growing hazard of container fires, a number of carriers have recently implemented fines on shippers who mis-declare hazardous cargo. Evergreen, OOCL and Hapag-Lloyd have all announced a range of fines to be implemented immediately.

Hapag-Lloyd is implementing a fine of US$15,000 per container for misdeclared hazardous cargoes, plus any costs required to mitigate the violation.

“Failure to properly offer and declare hazardous cargoes prior to shipment is a violation of the Hazardous Material Regulations. Such violations may be subject to monetary fines and/or criminal prosecution under applicable law,” Hapag-Lloyd announced.

Hapag-Lloyd holds the shippers liable and responsible for all costs and consequences related to violations, fines, damages, incidents, claims and corrective measures resulting from cases of undeclared or misdeclared cargoes.

Tom O’Malley, President and Founder of Florida-based TJO Cargo Insurance Owner, says that it is size that matters when making a decision about buying cargo insurance.

The more important question for a beneficial freight owner to ask themselves is how much money can they comfortably afford to lose at any one time? If you are a major international company then that number is fairly high. If you are not then the number may be a tad lower.

If once a month a shipper ships ten containers to China from the US valued at US$50,000 each container, the total risk exposure ceiling of physical loss of the cargo amounts to US$500,000 plus handling/disposal of damaged freight. It’s not all that impossible to accumulate value unintentionally. Today more than ever no matter how the containers are booked, they all may end up on the same mega vessel.

In the event US$500,000 is an acceptable loss for a shipper they can recover from and they can reship ten containers of inventory to replace the lost ten containers, and still have a happy day, they may question their desire to purchase cargo insurance. Over a long enough period of time, they will come out ahead if shipping standards remain high.

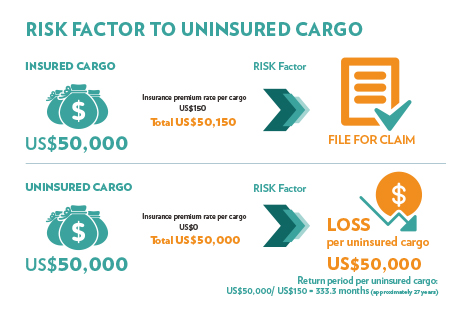

Let’s look at the pay back of not spending money on premiums if one of the example shipments does succumb to risk and is lost. For an insured example let us use a cargo insurance premium rate of US$150 for Clause A ‘all-risks’ insurance for a full container load of general merchandise valued at US$50,000 headed to China from the US.

For an identical uninsured example, the cargo insurance premium rate is US$0 for a shipment cost savings of US$150. For the insured shipment in the event the cargo is lost as a result of a covered peril, it would take the insured shipper a reasonable number of weeks to file and collect on a claim.

In the uninsured example, the shipper would have saved the US$150 premium per shipment but would have to continue to ship their monthly uninsured US$50,000 container a little over 27 years (333 months) to save as much premium money as to equal the lost uninsured amount. The 27 years of course being contingent on no more uninsured losses.

There are also other reasons why some shippers don’t purchase insurance.

The main one is that large shippers choose to self-insure, covering the costs of any losses and accepting the financial risk for losses incurred.

The recommended cargo insurance is known as International Chamber of Commerce (ICC) Clause A, or ‘all-risks’ which covers everything other than what the coverage excludes.

“While there are standard and situational ICC Clause A exclusions, the principle exclusions include the inherent nature of the goods, insufficient or inadequate packing, ordinary wear and tear, and consequential loss or loss of market.” told Forward with Toll news website.

According to O’Malley, while the type of cargo insurance coverage rarely changes, one significant change in recent years has been the proliferation of insurance providers in the market. Hence, shippers must ensure they perform adequate due diligence before taking out a policy.

“For many years, the primary outlets for cargo insurance have been insurance brokers and freight forwarders. Today, cargo insurance can also be purchased from many intermediary re-sellers and the carriers themselves.”

“Due diligence should include the actual insurer, ensuring they are rated ‘A’ by an organisation such as A.M. Best, which measures and reports the financial stability of insurers, in either the short or long term,” he said.

As the maritime insurance industry looks to increase its access to shippers and shipowners in China, a new online shipping platform has been launched to cater for the very large shipping cluster in the Greater Bay Area – which includes Hong Kong, Macau and nine other cities in Guangdong Province.

The focus of the new shipping insurance transaction platform will be research and development of the shipping insurance sector in South Mainland China.

Nansha, the business and shipping centre of Guangzhou, will be the centre of development for maritime, transportation, shipping exchange, ship finance, maritime services and shipping insurance, according to an article published in Seatrade Maritime News.

The platform is jointly set up by Shanghai Insurance Exchange, Guangzhou Shipping Exchange Company, PICC Property and Casualty Company Limited Guangdong Branch, China Ping An Property Insurance Guangdong Branch, China Pacific Property Insurance Company Guangdong Branch and China Dadi Property Insurance Guangdong Branch.

The decision not to insure ocean cargo is a gamble that many shippers are prepared to take, but one significant loss means that the small savings made on not paying insurance premiums are just a drop in the ocean compared to covering the entire cost of a lost shipment.